Navigating Personal Income Tax in Vietnam

HCMC – Paying Personal Income Tax (PIT) is one of the key financial obligations that employers and employees have in Vietnam. In this article, we attempt to clarify some of the key regulations and tax rates involved with the payment of PIT.

RELATED: Dezan Shira & Associates’ Payroll and Human Resources Services

RELATED: Dezan Shira & Associates’ Payroll and Human Resources Services

In general, a typical monthly salary package will include gross salary and mandatory social security. PIT is levied on the balance after deducting mandatory social insurance contributions. Companies conduct PIT finalization on behalf of their employees at the beginning of the year for taxable income arising from the previous year.

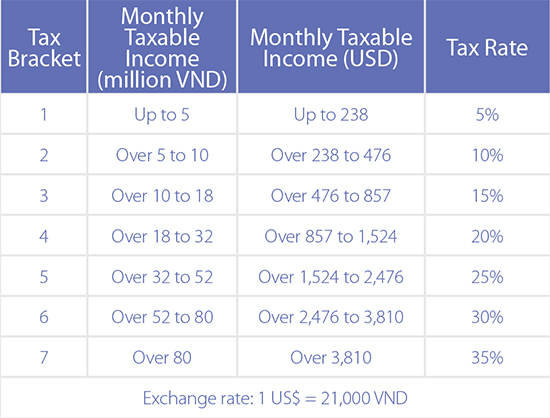

PIT rates for employment

Resident taxpayers are subject to PIT on their worldwide employment income, irrespective of where the income is paid or earned, at progressive rates from five percent to a maximum of 35 percent. Employment income includes salaries, wages, allowances and subsidies, remuneration in all forms; benefits earned for participation in business associations, boards of directors, control boards, management boards and other organizations; premiums and bonuses in any form except those received from the State. Non-resident taxpayers are subject to PIT at a flat rate of 20 percent on their Vietnam-sourced income.

It should be noted that the tax calculation and finalization procedures for Vietnamese locals and expatriates are the same; however, the procedures for residents and non-residents are different.

![]()

Understanding How to Hire and Pay Staff in Vietnam

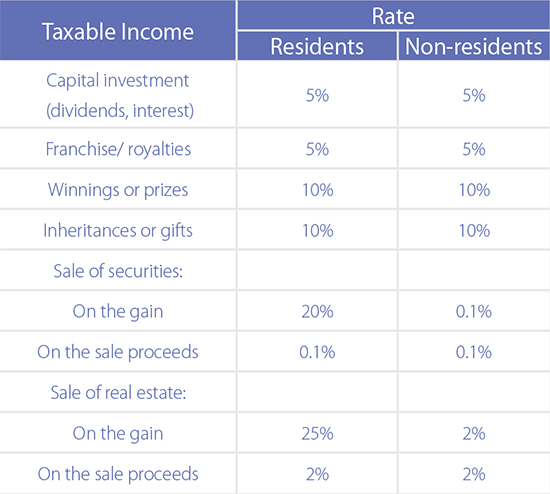

Taxable income

There are 10 types of earnings which are subjected to PIT as follows:

- Incomes from business activities

- Wages received from employers

- Capital investment

- Capital transfer

- Property transfer

- Prizes

- Royalties

- Commercial franchising

- Inheritances in forms of securities, capital contribution in companies or economic organizations, real estate and other assets requiring the registration of ownership or use right

- Gifts in forms of securities, capital contribution in companies or economic organizations, real estate and other assets requiring the registration of ownership or use rights

Are you a tax resident?

A resident is an individual satisfying one of the following conditions:

- Is staying in Vietnam for an aggregate of 183 days or more within one calendar year or a consecutive 12-month period from the first date of arrival; or

- Has a permanent residence that has been registered pursuant to the Law on Residence; or

- Has a leased residence to stay in Vietnam where the lease contract has a term of 90 days or more within the tax assessment year. Leased residences include hotels, boarding houses, rest houses, lodgings and working offices.

Foreign individuals can be exempted from taxation for certain benefits, such as:

- One-off relocation allowance for foreigners to relocate to Vietnam (based on the amount stipulated in the labor contract or agreement between the employer and the employee);

- Round-trip air fare paid once a year by employers for their foreign employees who are on annual leave (the air ticket should indicate the country where these employees are nationals or where the foreigner’s family lives); and

- General education school fees or tuition paid by the employer for the expatriates’ children studying in Vietnam (based on the invoice from the school and the labor contract).

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email vietnam@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

Vietnam: A Guide to HR in Asia’s Next Growth Market

Vietnam: A Guide to HR in Asia’s Next Growth Market

In this issue of Vietnam Briefing, we attempt to clarify human resources (HR) and payroll processes in Vietnam. We first take you through the current trends affecting the HR landscape and then we delve into the process of hiring and paying your employees. We next look at what specific obligations an employer has to their employees. Additionally, we guide you through the often complex system of visas, work permits, and temporary residence cards. Finally, we highlight the benefits of outsourcing your payroll to a “pan-Asia” vendor.

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Doing Business in Vietnam 2014 (Second Edition)

An Introduction to Doing Business in Vietnam 2014 (Second Edition)

An Introduction to Doing Business in Vietnam 2014 (Second Edition) provides readers with an overview of the fundamentals of investing and conducting business in Vietnam. Compiled by Dezan Shira & Associates, a specialist foreign direct investment practice, this guide explains the basics of company establishment, annual compliance, taxation, human resources, payroll, and social insurance in the country.

- Previous Article PIT Update: Vietnam Implements 50 Percent Reduction in Personal Income Tax for Individuals Working in Economic Zones

- Next Article Rahmenerweiterung der Einkommensteuer für ausländische Unternehmen in Vietnam